In the intricate dance of global finance, the phenomenon of tax havens occupies a central stage, intricately woven into the very fabric of capitalism. The capitalist system, with its relentless pursuit of profit maximization and competitive advantage, inadvertently cultivates an environment where tax havens flourish. This article delves deeply into the multifaceted relationship between capitalism and tax havens, exploring the motives, mechanisms, and consequences that characterize this dynamic interplay. Readers will encounter a comprehensive examination, rich with economic theory, historical context, and policy implications.

The Pursuit of Profit and its Role in Tax Haven Utilization

Capitalism, at its core, thrives on the principle of profit maximization. Businesses continuously seek to optimize their financial performance, experimenting relentlessly with strategies that reduce costs and amplify returns. One of the most alluring methods in this quest is the minimization of tax liabilities. Tax havens—a term denoting jurisdictions with low or zero tax rates, strict secrecy laws, and favorable legal frameworks—offer an ideal refuge for capital to evade higher tax burdens imposed by home countries.

The capitalist proclivity for high returns generates robust incentives for corporations and wealthy individuals to shift profits artificially into these low-tax jurisdictions. This practice, often conducted through sophisticated legal mechanisms known as transfer pricing or intellectual property licensing, allows multinational enterprises to reallocate earnings without corresponding economic activity. As a result, these entities can reduce their effective tax rate considerably, gaining a competitive edge over firms that adhere to traditional taxation regimes.

Globalization and the Amplification of Tax Haven Dynamics

The dawn of globalization has intensified the nexus between capitalism and tax havens. As firms expanded beyond national borders, the complexity of international finance grew exponentially. Transnational corporations (TNCs) command vast networks of subsidiaries and affiliates, enabling them to exploit jurisdictional disparities more effectively than ever before.

Globalization engendered a fiscal race to the bottom, where states compete aggressively to attract foreign investment by offering preferential tax treatment, regulatory leniency, or stringent confidentiality. This paradigm, often described as “tax competition,” has facilitated an expansion of the number and variety of tax haven jurisdictions. Consequently, businesses operate within an environment devoid of centralized tax authority, navigating a labyrinthine system that rewards ingenuity in fiscal arbitrage.

Types of Tax Havens and Their Strategic Roles

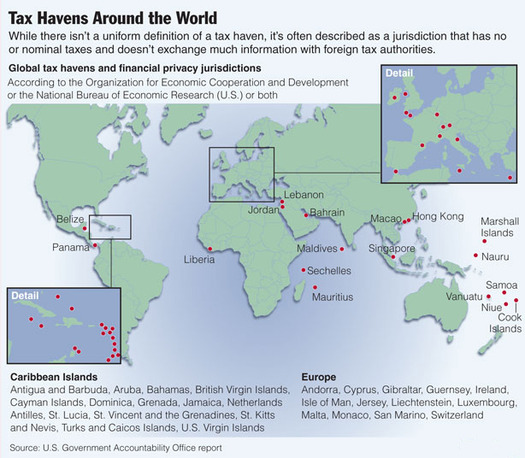

Tax havens are not monolithic; they manifest in diverse forms, each serving strategic roles within the capitalist ecosystem. Understanding these typologies enriches the dialogue on how capitalism perpetuates their viability.

- Financial Secrecy Jurisdictions: These havens, such as Switzerland or the Cayman Islands, provide robust confidentiality laws that shield beneficial owners from scrutiny. Capital flows into these territories, obscured from regulatory authorities, facilitating not only tax avoidance but also sometimes illicit activities like money laundering.

- Low or Zero-Tax Jurisdictions: Places like Bermuda or the British Virgin Islands offer extremely low corporate tax rates. This fiscal environment incentivizes companies to locate profits or even executive functions there, diminishing their global tax burden.

- Special Economic Zones and Offshore Financial Centers: These regions blend regulatory exemptions with advanced financial infrastructure, creating specialized ecosystems that attract complex financial transactions, including the establishment of shell companies and patent holdings.

The heterogeneity of these havens underlines capitalism’s adaptability, whereby actors select from a menu of options to optimize their fiscal positions according to evolving market conditions.

Regulatory Arbitrage and Capital Mobility

One of capitalism’s defining features is the unparalleled mobility of capital. Unlike labor, which is often tethered by geographical and social constraints, capital can be reallocated swiftly and strategically. This mobility fuels regulatory arbitrage—a tactic where businesses exploit discrepancies in national laws to circumvent unfavorable regulations or taxes.

Tax havens emerge as the quintessential manifestation of regulatory arbitrage. Corporations routinely channel funds through networks of subsidiaries in these jurisdictions to leverage gaps or weaknesses in international tax regimes. The efficacy of this strategy derives largely from the decentralized nature of taxation governance, wherein sovereign states guard their fiscal sovereignty yet inadvertently compete by lowering tax rates or altering regulatory parameters. Capitalism, in embracing market efficiency and competitive pluralism, thus enables and encourages these behaviors.

Economic Inequality and the Social Implications of Tax Havens

While the capitalist logic driving tax haven use centers on optimization and efficiency, the broader social and economic repercussions are profound. Tax havens contribute substantially to global economic inequality. By siphoning vast sums from fiscal coffers in higher-tax countries, they deprive governments of critical resources necessary for public goods and social welfare programs.

This erosion of the tax base exacerbates wealth disparities, as the state’s ability to redistribute income or invest in infrastructure weakens. The resultant gap between capital-owners and ordinary citizens intensifies, feeding cycles of disenfranchisement and social stratification. The capitalist system, by prioritizing private wealth accumulation often shielded behind offshore veils, thus indirectly perpetuates these inequities.

Capitalism’s Ideological Justifications for Tax Haven Use

The capitalist ethos often frames tax haven utilization as a legitimate exercise of economic liberty and corporate governance. Proponents argue that minimizing tax burdens is an exercise in fiduciary responsibility toward shareholders, enhancing shareholder value and stimulating investment.

Moreover, the rhetoric of deregulation and small government posits that lower taxation fosters entrepreneurship, drives innovation, and encourages economic growth. Within this ideological framework, tax havens are seen not merely as loopholes but as instruments to recalibrate the balance of power between the private sector and the state, privileging individualism and market freedom.

Responses and Future Outlook

In recent years, the global community has begun to grapple with the distorting effects of tax havens on both capitalist economies and tax fairness. Initiatives like the Base Erosion and Profit Shifting (BEPS) project by the OECD aim to close gaps and enforce greater transparency. However, the inherent tension between national sovereignty and global cooperation complicates these efforts.

The future trajectory of tax havens within capitalism depends largely on evolving international consensus and the willingness of states to reform fiscal policies. Technological advancements, such as blockchain and digital currencies, further complicate surveillance and regulation of cross-border capital flows, potentially intensifying the challenges.

Ultimately, capitalism’s intrinsic drive for efficiency and competitive advantage ensures that tax havens will remain entrenched within the global financial architecture unless comprehensive and coordinated systemic reforms are enacted.